This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

startled investors with a sharper-than-expected decline in profits and a gloomy outlook in its first earnings report since Chief Executive. Facebook also cited inflation as a weight on advertiser spending. and Canada, two of the company’s most profitable markets, the results show. Facebook parent. Meta Platforms Inc.

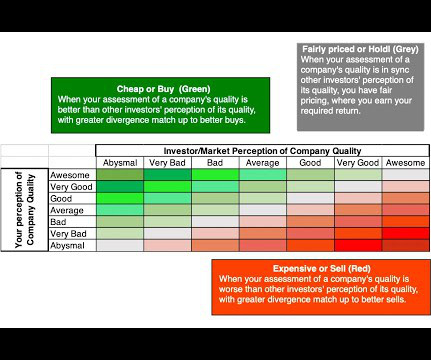

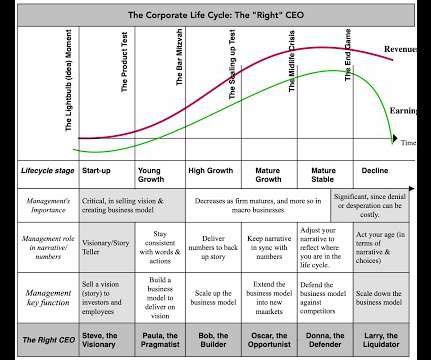

Operating Performance/Profitability Narrative : While it is easy to attribute rising stock prices entirely to mood and momentum, the truth is that momentum has its roots in truth. Money Machines : The pricing power and product demand resilience exhibited by these companies have manifested as strong earnings for the companies.

suffered the largest-ever loss. companies as they reassess their valuations in anticipation of higher interest rates. Amazon relieved investors with a near doubling in profit in the holiday period and said it is raising the price of its Prime membership in the U.S. AMZN 13.54%. company—just a day after Facebook parent.

Even people who are normally rational decision-makers can be prone to fear, greed, and overconfidence, and the persistence of market bubbles where investors chase whatever company or sector is all the rage at the time (and often get stuck with losses when the bubble pops) shows that herd mentality in investing is as prevalent as ever.

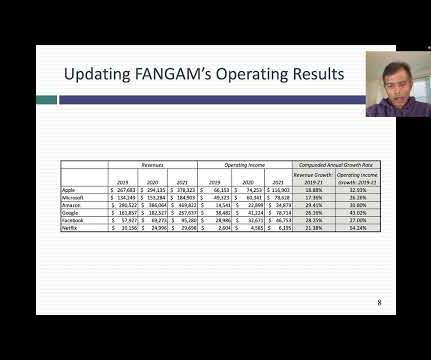

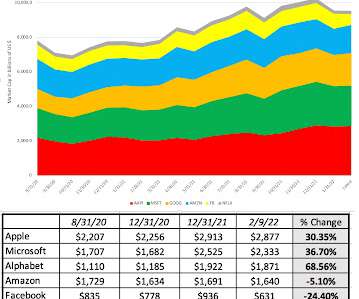

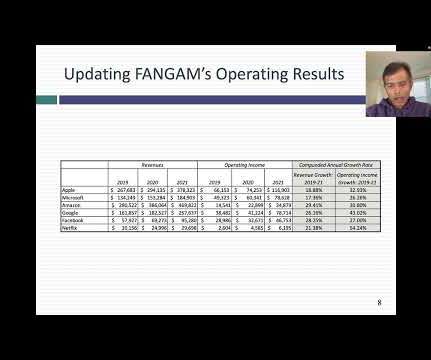

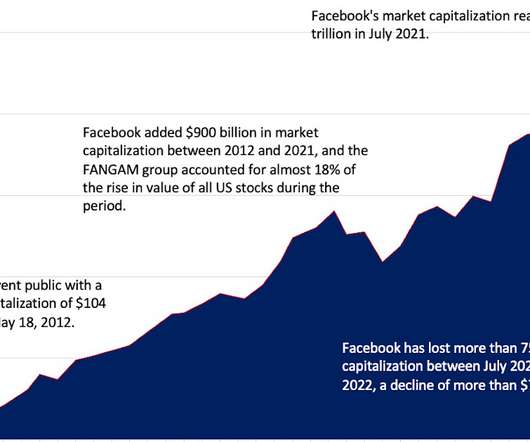

I must admit I was surprised by my own valuations, since, given the low riskfree rates prevailing at the time, only one stock (Apple) looked significant over valued. Clearly, much has happened since these valuations. trillion, and their share of the overall equity value of all US stocks also surged from 6.5% to 14.9%.

My September 2020 Valuations. I must admit I was surprised by my own valuations, since, given the low riskfree rates prevailing at the time, only one stock (Apple) looked significant over valued. Clearly, much has happened since these valuations. The FANGAM Valuations: February 2022. to 14.9%. Updating the Numbers.

The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies.

In the first, I will look at the grocery business, both in terms of growth and profitability of grocery stores, since Instacart, as an intermediary in the business, will be affected by grocery business fundamentals. On the profitability front, the grocery business operates on slim margins, at every level.

I must admit I was surprised by my own valuations, since, given the low riskfree rates prevailing at the time, only one stock (Apple) looked significant over valued. Clearly, much has happened since these valuations. trillion, and their share of the overall equity value of all US stocks also surged from 6.5% to 14.9%.

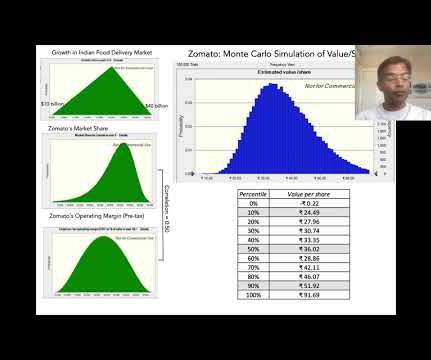

The primary attraction of the company, to investors, comes not from its current standing (modest revenues and big losses), but from its positioning to take advantage of the potential growth in the Indian food delivery market.

In the next post, I will use Facebook’s most recent earnings surprise to talk about inconsistencies in how accountants categorize corporate spending, and why these inconsistencies can skew investors perceptions of corporate profitability and financial health. billion in the third quarter of 2022. .

In the next post, I will use Facebook's most recent earnings surprise to talk about inconsistencies in how accountants categorize corporate spending, and why these inconsistencies can skew investors perceptions of corporate profitability and financial health. billion in the third quarter of 2022.

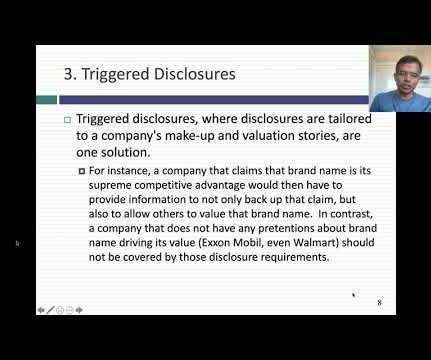

It extends into materiality, by reframing that concept in terms of value, rather than profits, and connecting it to disclosure, with disclosure requirements increasing proportionately with the value effect. Many subscription companies explicitly disclose contribution profits (e.g., StitchFix).

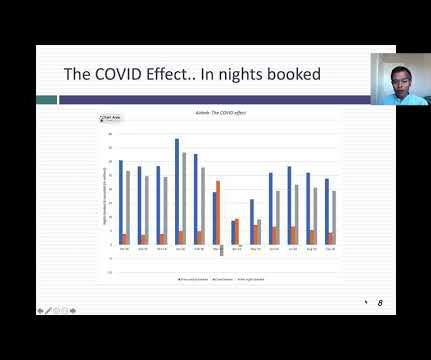

Setting the Table As with any valuation, the first step in valuing Airbnb is trying to understand its history and its business model, including how it has navigated the economic consequences of the COVID. In addition, growth in the experiences business will also push this metric upwards, since Airbnb keeps a 20% share of those revenues.

From 2001 to 2020, revenue growth at semiconductor businesses has dropped to single digits, as higher demand for chips in new uses has been offset by loss of pricing power, and declining chip prices. Sustained Profitability, with Cycles! While revenue growth has picked up again in the last three years, the business has matured.

Barry Ritholtz : Now, if I remember correctly, late nineties cracks in the facade were already showing of, you know, the, the monolithic radio, TV advertising world. I got the sense that, so Churnin takes 51% for a fairly modest valuation, 10 or $15 million. Big advertisers would never give Barstool Sports a look the way they do now.

But in the New York Times, there was an advertisement that the value line investment survey needed analysts. They announced a $640 million loss and ouch. But if, if it has a history of not being profitable, you you really want to exclude that. The visibility on earnings they grew but they stayed profitable as, as they grew.

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

Blue-collar workers in developed markets : The flip side of the rise of China and other countries as manufacturing hubs, with lower costs of operation, has been the loss of manufacturing clout and jobs for the West, with factory workers in the United States, UK and Europe bearing the brunt of the cost.

And, you know, therein began, I think the unraveling and, and a little bit of the, the loss of that, you know, cultural juice that had kind of historically made that firm special. And when we experience a loss, right, a 50% loss can happen right? I don’t wanna experience loss. We have that, those options as well.

ASNESS: Some of the things like betting against beta, quality or profitability, carry strategies were additions over time. ASNESS: And we had a great almost a decade, because everything else we do work, profitability one; fundamental, momentum one; low risk one. ASNESS: There are a few reasons. RITHOLTZ: Okay. RITHOLTZ: Past decade.

Now you have to assume some losses. Barry Ritholtz : And these bonds are still profitable Jeffrey Sherman : And they don’t break, like they, they don’t, they don’t, they don’t lose money, especially at 50 cents on dollar. And you know, it’s the same thing when valuation gets outta control too.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content