This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

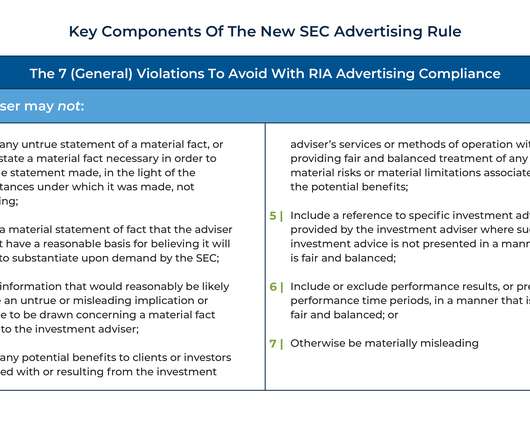

For investment advisers looking to attract prospective clients, advertising the performance of their investment strategies would be a logical way to market their services (at least if they had strong historical returns!). Two final prohibitions under the Marketing Rule include restrictions on the use of predecessor performance (e.g.,

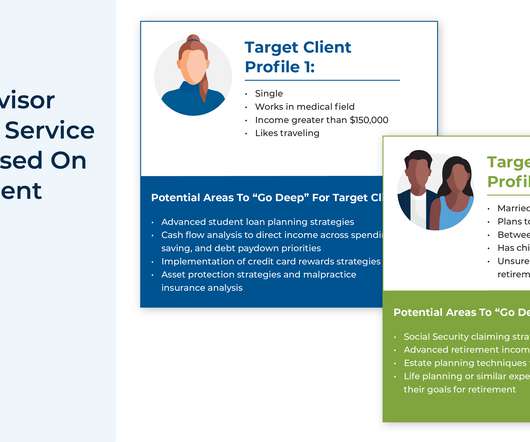

By applying the ideal-target-client framework, advisors can not only better target their marketing efforts (as they can align their website and other advertising efforts with their ideal client’s needs), but they can also streamline their day-to-day work, as they will encounter fewer ‘new’ issues as their client base grows.

Outside of work, he serves as a volunteer financial planner and class instructor for non-profits in the Northern Virginia area. He previously worked at a financial planning firm in Bethesda, Maryland, and as a journalist covering the banking and insurance industries. He can be reached at [email protected]. Read more of Adam’s articles here.

He has absolutely crushed his benchmark over that period. He’s crushed the Russell 2000, whatever benchmark you want to talk about. But in the New York Times, there was an advertisement that the value line investment survey needed analysts. They announced a $640 million loss and ouch. a year since 1989. Real money.

But if you buy low multiples and sell high multiples, either in a long-only beat the benchmark sense, whether over and underweight, and you did the same thing everyone does and call me a hedge fund manager. And value and momentum do, whether it’s relative outperformance against a benchmark or absolute performance in a hedge fund.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content