This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Role of IFRS in Simplifying Cross-Border Financial Reporting In todays interconnected world, businesses are no longer confined by borders. This is where International Financial Reporting Standards (IFRS) come into play. But what does it really mean to be IFRS-compliant? What is IFRS Compliance? Why is it important?

For example, while South African companies follow International Financial Reporting Standards (IFRS), the US requires compliance with its Generally Accepted Accounting Principles (GAAP). IFRS is principles-based and allows for some judgment in financial reporting, while GAAP is more rigid, rules-based, and less forgiving.

Financial reporting specialist and lecturer Adam Deller explains the basic principles of IFRS 5, 'Non-Current Assets Held for Sale and Discontinued Operations'. The post The fundamentals of IFRS 5 appeared first on FutureCFO.

Financial reporting specialist and lecturer Adam Deller explains the basic principles of IFRS 16, Leases. The post The fundamentals of IFRS 16 appeared first on FutureCFO.

The consolidation process typically includes aggregating financial results, eliminating intercompany transactions, handling currency conversions, and ensuring compliance with accounting standards like the International Financial Reporting Standards (IFRS) or Generally Accepted Accounting Principles GAAP.

IFRS 9 is changing hedge accounting forever. Companies in the European Union have only begun to kick off their IFRS 9 initiatives since the European Commission endorsed the standard in November 2016. IFRS 9 Advantages in a Nutshell. Under IAS 39, many hedges that did not qualify for hedge accounting may qualify now.

Its not merely numbers on a page but its the heartbeat of accountability and the foundation of trust with external stakeholders, particularly investors. In 2014, an accounting error resulted in the company overstating its income by R849 million. Cloud based automation platforms that easily sync with ERP and accounting systems.

Previous posts in this blog series o n Environmental, Social and Governance (ESG) and carbon accounting have spotlighted carbon accounting as a trend to watch , looked at ESG impacts on M&A , and tracked the emergence of new ESG standards.

Navigating IFRS , Key Updates and Changes Introduction In today’s fast-paced financial world, staying up to date with the latest International Financial Reporting Standards (IFRS) is critical for CFOs. IFRS 16 Leases: Impact on Balance Sheets IFRS 16 has changed the way leases are recorded on balance sheets.

Financial reporting specialist and lecturer Adam Deller explains the basic principles of IFRS 9, Financial Instruments. The post The fundamentals of IFRS 9 appeared first on FutureCFO. First published on Youtube.

The Financial Reporting Council (FRC) calls for IFRS 17 disclosures improvements in its recently published IFRS 17 'Insurance Contracts' thematic review. The IFRS 17 disclosures improvements that FR C expects include the following. The post IFRS 17 disclosures improvements needed: FRC appeared first on FutureCFO.

IFRS 17 will change insurers' reported earnings and equity as it alters their profit recognition patterns and measurement of liabilities, while not directly affecting insurers' creditworthiness, said Moody's recently. The post IFRS 17 won't directly affect insurers' creditworthiness appeared first on FutureCFO.

One of the major IFRS 17 challenges is that it’s disrupting business as usual for insurers. According to a WTW IRS 17 survey, there are major post-implementation challenges that insurers still need to overcome after reporting their half-year 2023 results under IFRS 17 for the first time.

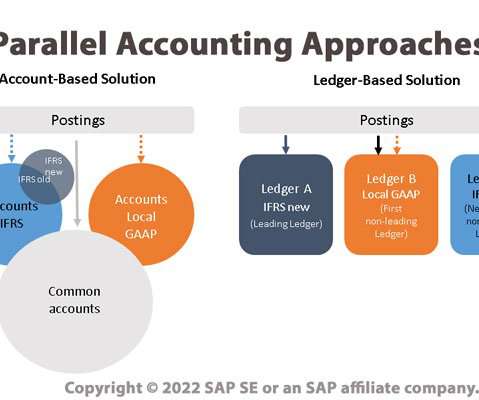

One important side effect of the ongoing trend toward globalization is the need to comply with a range of different accounting principles as well as with disparate reporting and compliance mandates. Parallel Ledgers - in which multiple ledgers are used, with an accounting principle applied to each ledger.

Insurers have reported that there is still a huge amount of work to complete in order to successfully deliver IFRS 17 ahead of the 2023 deadline, said WTW recently. According to WTW’s latest survey, entitled ‘IFRS 17: Will we make it?’, insurers report material progress has been made since WTW’s previous IFRS 17 poll in 2021.

Since the release of new lease accounting standards ASC 842 and IFRS 16 in 2018, companies have taken a variety of approaches to comply, but many are now aiming to optimize their lease accounting processes for efficiency and long-term manageability. Register Now!

IFRS 16, published by the International Accounting Standards Board (IABS), came into effect on January 1, 2019. In an effort to boost transparency, IFRS 16 eliminates the distinction between finance leases, which were previously capitalized on corporate balance sheets, and operating leases, which were not.

Financial reporting specialist and lecturer Adam Deller explains the basic principles of IFRS 8, Operating Segments. The post The fundamentals of IFRS 8 appeared first on FutureCFO.

AI in the “Real World” While these powerful tools seem to have a near mastery of natural language communication, they are not necessarily designed to possess many of the skills required by finance and accounting professionals. However, they still have a place in corporate finance and accounting.

This new post provides a deeper look at how the leasing of medical equipment along with other bundled services or products presents particular challenges for meshing contracts and lessor accounting with DSE management and revenue recognition. For revenue recognition, they also must comply with ASC 606 and IFRS 15. billion by 2032."

Chinese Study highlights limitations on IAS 38, accounting for intangible assets A recent study from China highlighted the limitations of IAS 38 —the International Accounting Standard that governs intangible assets—and its impact on innovation, particularly in high-tech industries.

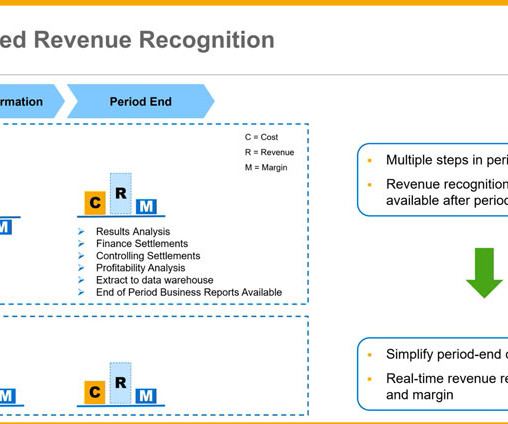

Over the past eight years, many episodes in this blog series have focused on revenue recognition and how SAP solutions such as Revenue Accounting and Reporting (RAR) have provided a robust foundation for compliance with ASC 606 and IFRS 15.

In the third of EY's Global IFRS video series on the implementation of IFRS 16, Emily Moll and Victor Chan discuss agenda decisions reached by the IFRS Interpretations committee about the application of IFRS 16. The post IFRS Interpretations Committee agenda decisions on IFRS 16 (I) appeared first on FutureCFO.

Delay in FX hedging, accounting treatment. The accounting treatment of currency hedging (timing) mismatches remains a major problem that has become more acute in the wake of the health crisis. Accounting consequences of hedging adjustments. Cash-Flow Hedge (CFH) Method applied. TMS), and shifted in time.

As the world has become more serious about mitigating climate change and the issue of corporate responsibility moves to the forefront, ESG reporting is now shifting toward a more rigorous approach that is increasingly based on accounting disciplines and auditable practices.

Why Maake believes Treasury was right A core point of Maake’s argument is that State Owned Companies (SOCs) like Eskom are expected to not only adhere to IFRS and the Companies Act, but also the PFMA. All these elements are covered under IFRS. But there must be an alternative way of making management to be accountable.”

Financial Information Systems help businesses automate compliance checks, ensuring they meet regulations such as International Financial Reporting Standards (IFRS 17) and tax laws. This means decisions can be made quickly, without waiting for accountants to prepare reports.

After several months of re-deliberations, the International Accounting Standards Board (the Board) has published the final amendments to IFRS 17 Insurance Contracts. The post IFRS 17: Final amendments are out now appeared first on FutureCFO.

This important issue was previously explored last year in Are You Ready for "Carbon Accounting" Compliance? A subsequent blog post specifically addressed How Can Carbon Accounting Impact the Value of M&A Deals? ISSB was established by the IFRS Foundation in response to the Glasgow COP 26 conference in November 2021.

Financial reporting specialist and lecturer Adam Deller explains the basic principles of IFRS 2, “Share-based Payment”, in this short video. The post The fundamentals of IFRS 2 appeared first on FutureCFO.

Choosing the right accounting software is important. Financial governance allows your organization to meet compliance requirements, such as IFRS and GAAP updates, by having the right financial controls in place. However, there are exceptional cloud accounting software programs that can take that complexity and make it simple.

However, amidst the ever-expanding role of the Office of the CFO, accounting still is a major responsibility and this arena also is radically changing with the availability of new tools, technologies and challenges. These capabilities address key operational accounting issues as companies transform their business offerings.

This video considers the accounting for the latest IBOR reform developments, as entities transition their exposures to risk free rates. The post IFRS Video: IBOR reform, year-end considerations appeared first on FutureCFO.

Written by Leigh Schaller “Growing up in my dad’s business, accounting was natural for me. In high school, I always received the accounting awards. It was a natural progression into the accounting industry,” Ehsaan Moosa, told the CFOClub podcast. He recently shared with CFOClub the knock on effects of load shedding.

In this episode, EY Global covers the key reminders and considerations about the implementation of IFRS 16 Leases by lessees as calendar year-end entities finalise their annual financial statements. The post IFRS 16 Leases: Key issues and challenges appeared first on FutureCFO.

The post Global IFRS: IBOR transition discussions appeared first on FutureCFO. Tony Clifford and David Bradbery from EY talk through the tentative decisions taken in January 2020 by the IASB for their IBOR reform project.

Driven by sweeping changes such as digital transformation, globalization of markets, the subscription-based Digital Solutions Economy™ (DSE), carbon-accounting mandates, a rising emphasis on artificial intelligence, and other disruptive trends, the role of Chief Financial Officer (CFO) is undergoing radical transformation too.

In the second of our Global IFRS video series on the implementation of IFRS 16, Emily Moll and Victor Chan discuss a recent survey on the disclosure of the expected impact of adopting IFRS 16 on the date of initial application by large entities.

Follow standard accounting rules In most industries, this means using IFRS (International Financial Reporting Standards) or IFRS for SME (International Financial Reporting Standard for Small and Medium-sized Entities) to prepare financial statements.

Certified Professional Accountants (CPAs) in California are calling on an industry watchdog to clarify standards for cryptocurrency accounting, with expectations that corporations will increase their use of cryptocurrencies moving forward. GAAP,” the letter stated.

The CFO Forum and Insurance Europe—representing 23 of the continent’s largest insurers and 95% of premium income—call for a delay of the IFRS 17 implementation deadline to Jan 1, 2023. According to the letter, the organizations also asked for additional changes to IFRS 17.

The survey was conducted to learn more about emerging presentation and disclosure practices, as well as the transition effect of IFRS 15 on entities in selected sectors. The post Overview of EY IFRS 15 presentation and disclosure survey appeared first on FutureCFO.

This latest installment in our ongoing DSE blog series takes a step back with a holistic look at the entire order-to-cash process and explores how revenue accounting compliance can seamlessly integrate with DSE. Manual interventions needed for tracking and accounting for subscription revenues. Complex allocations of revenue.

In this video Tony Clifford, Jane Hurworth and David Bradbery discuss some practical issues in applying the IFRS IBOR reform amendments, with some illustrative examples. The post Global IFRS video: Applying the IBOR reform amendments in practice appeared first on FutureCFO.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content