This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

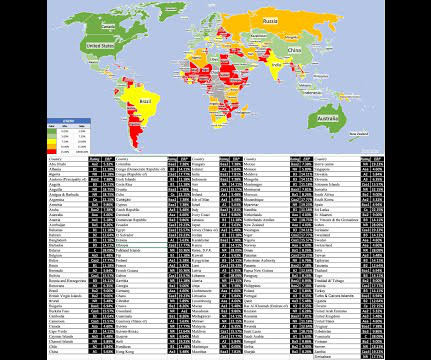

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

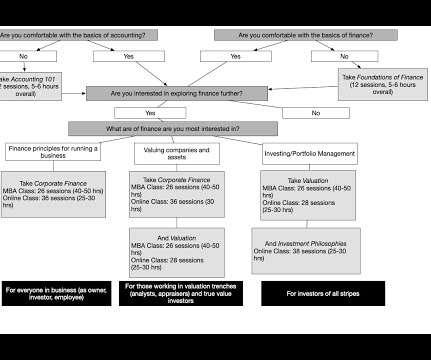

I am in the third week of the corporate finance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet. It is for that reason that I created my own version of an accounting class , that you can find on my webpage.

The question of whether a company is making or losing money should be a simple one to answer, especially in an age where accounting statements are governed by a myriad of rules, and a legion of number-crunchers follow these rules to report profits generated by a firm. The numbers yield interesting insights. .

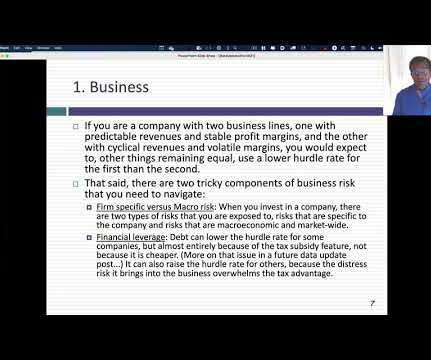

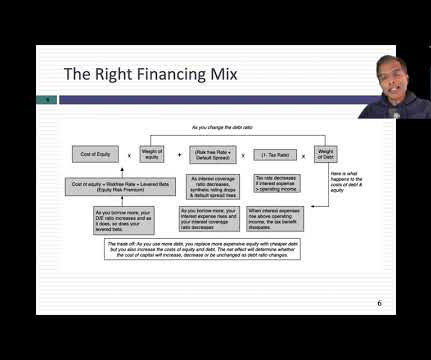

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

Measuring Profitability The question of whether a company is making or losing money should be a simple one to answer, especially in an age where accounting statements are governed by a myriad of rules, and a legion of number-crunchers follow these rules to report profits generated by a firm. The numbers yield interesting insights.

Mean reversion : I am not a knee-jerk believer in mean reversion, but the tendency for numbers to move back towards averages is a strong one. Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all.

The numbers that I computed opened my eyes to how much perspective on the high, low, and typical values, i.e., the distribution of margins, helped in valuing the company, and how little information there was available, at least at that time, on this dimension. Aggregate operating numbers 3. Insider, CEO & Institutional holdings 2.

Cash Return in 2024 Let's start with the headline numbers. Breaking down global companies by region gives us a measure of variation on cash return across the world, both in magnitude and in the type of cash return: It should come as no surprise that the United States accounted for a large segment (more than $1.5

Implementing DTSCF can be more complex than traditional SCF due to the increased number of parties involved and the need to track payments across multiple tiers. In DTSCF, large corporations extend financing beyond their immediate tier 1 suppliers to those suppliers suppliers (tiers 2, 3, and beyond).

Setting the Stage The notion of a business life cycle is neither new nor original, since versions of it have floated around in management circles for decades, but its applications in finance have been spotty, with some attempts to tie where a company is in the life cycle to its corporate governance and others to accounting ratios.

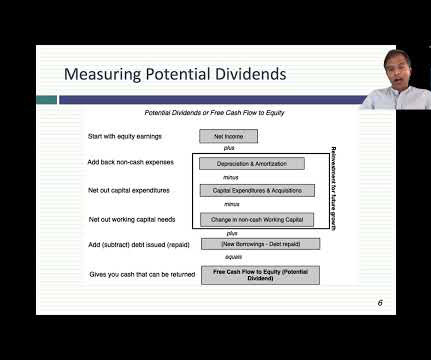

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

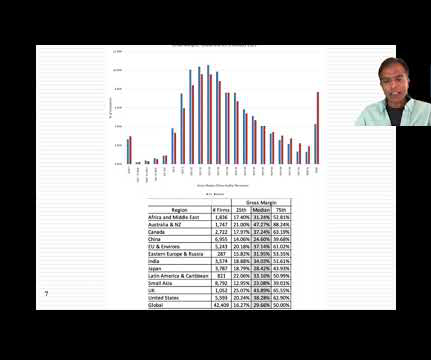

Starting with gross margins, and computing the number for all non-financial service firms, we report the distribution of gross margins across publicly traded companies at the start of 2023, again based upon gross income and sales in the most recent twelve months: While the median gross margin across all publicly traded global firms is about 30%.,

Mean reversion : I am not a knee-jerk believer in mean reversion, but the tendency for numbers to move back towards averages is a strong one. Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all.

He co-chairs a number of the asset management investment committees. And my dad had always said, as many young kids get this advice, doctor, lawyer, accountant, engineer. SALISBURY: And accountant seemed like a reasonable option. And I kind of stumbled my way into accounting. What can I say about Julian Salisbury?

In closing, I also want to dispense with the notion that data is objective and that numbers-focused people have no bias. Finally, it is worth noting that, notwithstanding the travails of last year, the number of firms in the data universe increased from 44,394 firms at the start of 2020 to 46,579 firms, a 4.9%

” look at the Monte Carlo simulations, look at what is the hurdlerate. But we want it on the calendar so that we keep clients and ourselves accountable so that we make sure that those meetings actually do happen. And so, that can move the numbers, as well. Did things change significantly since we updated the plan?,”

Last week, was my data week, where I download and analyze data on all publicly traded companies, listed anywhere in the world, and I will post extensively on what the numbers look like after a most tumultuous year. As we approach the turn of the calendar year, I have my own set of rituals that prepare me for the new year.

BUCKLEY: They were all institutional separate accounts. We’ve always been a virtual company, just used to be through the mail and 1-800 number when I joined. So that’s a number I hadn’t seen before. Number one, you put it back into the business. That means a low hurdlerate. RITHOLTZ: Wow.

Furthermore, do they optimize they debt ratios to deliver the lowest hurdlerates. Book versus Market : The book debt ratio is built around using the accounting measure of equity, usually shareholder's equity, as the value of equity. Do companies optimize financing mix?

The failures of the signal have been variously attributed to low interest rates, accounting mis-measurement of earnings (especially at tech companies), and by some, to animal spirits. Data Update 4 for 2021: The HurdleRate Question. Data Update 2 for 2021: The Price of Risk!

So, you’ll see that in this sort of what you might call a proto capitalistic society, interest is serving a number of different important functions. Well, the way I see negative rate is it’s a tax on capital, which is instituted by an unelected — RITHOLTZ: Central bank.

In particular, there are wide variations in how risk is measured, and once measured, across companies and countries, and those variations can lead to differences in expected returns and hurdlerates, central to both corporate finance and investing judgments.

The graph below shows the sovereign CDS levels, by country: Source: Bloomberg ( July 2023 data ) There are three things to note, as you browse these numbers. That said, there is no intellectual firepower or research behind these numbers, since I am letting the default ratings agencies and risk measurement services carry that weight.

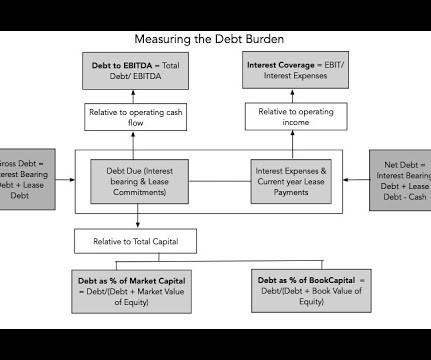

There are many who trust accountants to do this for them, using whatever is listed as debt on the balance sheet as debt, but that can be a mistake, since accounting has been guilty of mis-categorizing and missing key parts of debt. to3.5%) during the year.

So it’s got this math angle where it, you know, it’s all numbers, but then there’s this behavioral angle and psychological angle where, you know, it’s, it’s kind of a fun problem to tackle. It’s kind of a silly number, but people are going to think you’re smart or dumb based on that number.

Honest back testing, really looking at the numbers versus exaggerating returns and, and making up the claim that something’s live when it’s not. 12, 14 even that not a lot of numbers. So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers.

And 00:06:38 [Speaker Changed] Door number one was much better than door number three in, in the circumstances. Accounting was very difficult. It’s about a 50% fail rate, something like that. When we talk about breadth, we’re talking about the numbers of advancers versus decliners. Maybe even more.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content