This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

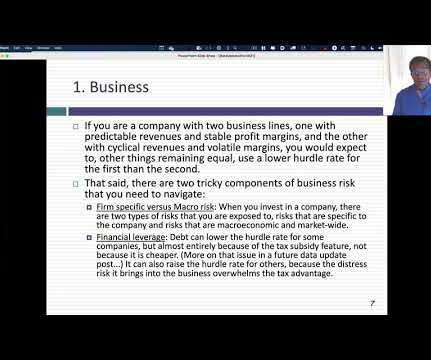

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

Financial institutions can better understand the risk profiles of small suppliers by leveraging alternative data and machine learning, thus expanding access to financing. It requires accurate data, robust technology, and thorough risk assessment, crucial to ensuring the creditworthiness of suppliers at all levels.

When valuing or analyzing a company, I find myself looking for and using macro data (risk premiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. Thus, market capitalization, interest rates and risk premiums, the data is as of that date.

Setting the Stage The notion of a business life cycle is neither new nor original, since versions of it have floated around in management circles for decades, but its applications in finance have been spotty, with some attempts to tie where a company is in the life cycle to its corporate governance and others to accounting ratios.

When valuing or analyzing a company, I find myself looking for and using macro data (risk premiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. Per-employee Statistics Profitability Financial Leverage Reinvestment 1. Bond Default Spreads Growth RatesAccounting Clean up Tax Rates 1.

BUCKLEY: They were all institutional separate accounts. But the true change comes when, hey, you know what, those loyal to that technological change figure out over not one, two, but three, five years, how to drive change and how to leverage it. That means a low hurdlerate. RITHOLTZ: Billion with a B. RITHOLTZ: Wow.

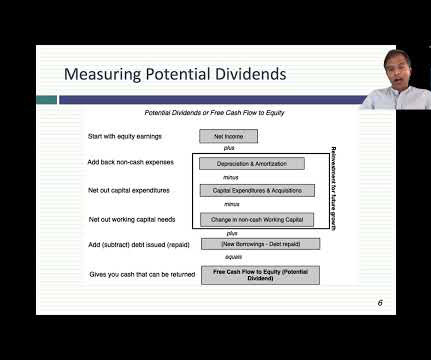

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

You do the math and you’re like, “Okay, well, an advisor can handle about 100 clients, an associate advisor can help with some of those clients, you can leverage maybe an associate advisor with a couple of advisors, but there’s a capacity limit for each of the roles.”

In fact, that may explain why firms that trade at low EV to EBITDA multiples are more likely to become targets in leveraged buyouts (LBOs) or leveraged recapitalizations. Business risk : Not surprisingly, for any given level of cash flows and marginal tax rate, riskier firms will be capable of carrying less debt than safer firms.

And my dad had always said, as many young kids get this advice, doctor, lawyer, accountant, engineer. SALISBURY: And accountant seemed like a reasonable option. And I kind of stumbled my way into accounting. That background of being an accountant was just great bedrock training. RITHOLTZ: Sure. Very different fields.

I mean, I didn’t want to blow my own trumpet up too much because most of the positions were in place, the quality funds, which more defensive and less leveraged, and low allocation to — a relatively low allocation to equities, and then the hedge funds sort of long/short positions that benefited in the financial crisis.

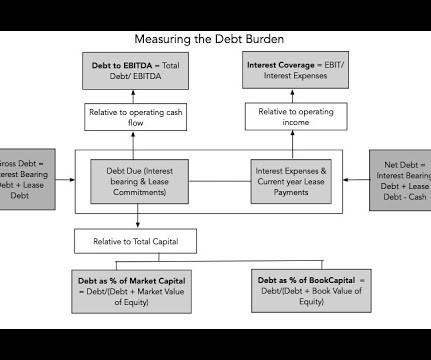

There are many who trust accountants to do this for them, using whatever is listed as debt on the balance sheet as debt, but that can be a mistake, since accounting has been guilty of mis-categorizing and missing key parts of debt.

So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. This is implicitly leverage. Leverage is a tool that accentuates both the good and the bad. And you need to be aware of the leverage risk that’s embedded. The second is behavioral.

Accounting was very difficult. It’s about a 50% fail rate, something like that. 00:26:19 [Speaker Changed] It, it’s, it’s usually it is aggressive shorts from leveraged funds on s and p futures. And I remember that first level was tough. I had no finance background. So, 00:08:16 [Speaker Changed] Right.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content