This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And while the coronavirus pandemic has thrust traditional B2B suppliers into a state of uncertainty, Spear noted that there are opportunities to emerge from the volatility by transforming accounts receivable (AR) and trade credit processes. B2C Sellers’ B2B Incentive. Optimizing Ad-Hoc Procurement.

Last week, the Fed’s Secure Payments Task Force called for comment from industry stakeholders about what challenges they face when it comes to payments security. “The Secure Payments Task Force is particularly interested in understanding any barriers that may exist to implementing the planned solutions.”

Sector-Specific Dynamics Several sectors showed notable trends in 2024: B2B remained the largest target for middle-market PE, accounting for 37.1% B2C experienced a resurgence, with deal volumes climbing 10.9% The window for action is narrow, and the firms that move decisively will secure the best outcomes.

Cybersecurity returned to the top of the B2B startup investment list as three companies in the enterprise security realm landed nearly half of the $246 million in B2B venture capital this week. Cequence Security. Also operating in the enterprise security space is Cequence Security, based in California. Contrast Security.

Moving from paper to digital has evolved for business-to-consumer (B2C) payments in recent years, but upgrading business-to-business (B2B) payments has taken longer. There are more tools available than ever to help SMBs move their accounts payable (AP) and accounts receivable (AR) processes forward to become more efficient.

According to Viewpost CEO Max Eliscu, B2B payments often follows in the same footsteps as B2C. The future of the payments industry is highly dependent on leveraging innovation like biometrics, data integration and a growing variety of payment methods to securely drive more volume with visibility, speed and simplicity.”.

Today in B2B, Bloomberg broadens its credit risk data pool, and two ERP solutions secure B2B payments integrations. Everlink, FINTAINIUM Team Up To Offer Real-Time B2B, B2C Payments. Palette Software has connected its accounts payable (AP) automation cloud technology with Aptean ERP , according to a Monday (Nov.

Sector-Specific Dynamics Several sectors showed notable trends in 2024: B2B remained the largest target for middle-market PE, accounting for 37.1% B2C experienced a resurgence, with deal volumes climbing 10.9% The window for action is narrow, and the firms that move decisively will secure the best outcomes.

Disruption is hitting both the B2C and B2B arenas, and while it would seem they are two opposite ends of the spectrum, these ecosystems share commonalities in the kinds of trends that force sellers to modernize their market strategies. Treasury is very well-positioned to handle all of these activities,” added Sinha. trillion by 2021.

Most consumers are very surprised by the degree to which their banks are not using location to keep their accounts safe.” . Chief security officers and most FinTech space players would typically say they already look at geolocation as part of their risk scoring, considering it critical to their fraud detection efforts.

That includes using technology to take the notion of simply moving money from one country to another to a new level, including sowing the seeds for the ignition of a real-time global, mobile P2P network that offers senders and receivers optionality, convenience and security. In markets, banks need to drive affinity to their brands.

They can eliminate the pain points in business-to-consumer (B2C) transactions by keeping consumers from waiting to receive their funds, while businesses are witnessing the advantages of using real-time payments when transacting with each other. Stronger security strategies and solutions could help turn the tide and boost adoption.

The outmoded B2B payments landscape stands in stark contrast to the business-to-consumer (B2C) and peer-to-peer (P2P) spaces where instant money and real-time payments are becoming the norm. It works both ways as traditionally B2C sellers dip their toes into lucrative B2B waters. Keeping B2B Payments Honest.

However, B2B payments are not the same as B2C, largely thanks to high transaction sizes and volumes, as well as expanding fraud risks. Traditionally, accountants and their SMBs have to access separate platforms, be it other payment or online banking portals, to initiate payment.

Entryless, a cloud-based financial network that allows small and medium-sized businesses to react more quickly to the needs of their buyers and suppliers, announced an integration with accountancy platform Sage Live. This integration will improve companies’ ability to pay bills and complete accounts seamlessly.

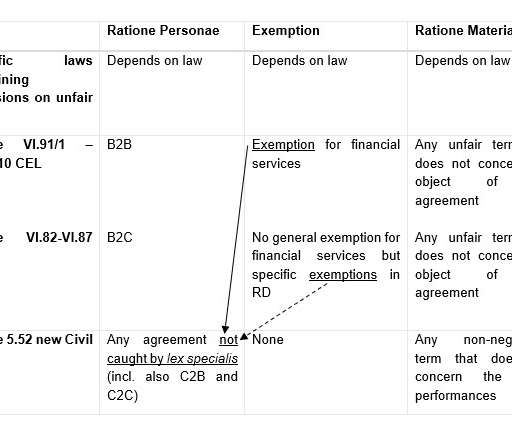

Before that, the B2B and B2C legislation had already introduced a similar prohibition, but financial services had been (partially) exempted. of the new Civil Code, the B2B and the B2C regime. The assessment of the manifest imbalance takes into account all circumstances around the entry into the agreement. Article 5.52

Being able to track the flow of funds and correctly auto-post those funds to an invoice-level based accounts receivable (AR) system, said Diegelman, can be difficult. He noted that with rates being as volatile as they’ve been of late, time in this instance is literally money for consumers, possibly quite a lot of it.

Yet, as Tony Horling, founder and CEO of InTu Mobility , recently told PYMNTS, mPOS technologies designed for business-to-consumer (B2C) payments won’t cut it for multibillion-dollar enterprises that need to accept B2B payments in the field. Benefits For Payers.

While the business-to-consumer (B2C) eCommerce boom has arguably already occurred, the global pandemic is introducing a second wave of digital commerce adoption. But this isn't a trend reserved for the B2C space anymore. But this isn't a trend reserved for the B2C space anymore.

PayPal and HSBC share a common vision of making payments simpler, secure and more convenient for merchants and consumers who want to manage and move their money digitally around the globe.”. The tie-up integrates PayPal with Bank of America’s Global Digital Disbursements solution that supports business-to-consumer (B2C) global payments.

Accounts payable (AP) departments were no longer in the office to cut paper checks, and accounts receivable (AR) personnel were no longer in the office to receive them. For some B2C firms, that meant expanding into the B2B market.

Just as in other markets, eChecks, ACH, paper checks, wires and credit cards all come with their various benefits, as well as their pain points, from high processing fees to a lack of security. To solve for this, AeroPay recently launched its cannabis-targeting payments solution designed for both B2C and B2B payments.

.” The SAP add-on assists with digital payment types that have to comply with the Payment Card Industry Data Security Standard (PCI DSS). ” SnapPay handles the accounts receivable (AR) and accounts payable (AP) processes of large and mid-sized companies. The solution also computerizes corporate treasury operations.

Between data breaches exposing customer details and card information and the rise of card-not-present fraud as operations move online, digital businesses are challenged to stay abreast of payment security trends — and fraud is a massive issue for firms large and small. This isn’t merely an issue for the B2C world, however.

But onboarding isn't just about obtaining bank account or payment details of a potential buyer. That's one thing where B2C selling merchants can learn from B2B selling merchants. There are many ways that onboarding a new B2B customer can be a headache for suppliers that sell goods and services online.

Artificial intelligence-powered tools, like virtual assistants, have the potential to reduce the time it takes to close the books from 10 days to just two, placing the remaining eight days in the hands of accountants and other finance chiefs to wield more strategically for their enterprise. in particular.

WannaCry’s explosive impact on the industry has enterprise security on everyone’s mind, and this startup is now a unicorn because of that attention, closing $100 million in Series D financing. The company revealed Crosslink Capital led the funding, which also saw participation from Talis Capital and Enterprise Security Syndicate.

Unlike simpler more streamlined business-to-consumer (B2C) purchasing, B2B sellers still ship goods or extend services on the promise of being paid later on an unspecified date, usually months. Where’s the Trust? The speed of payments relies at some point on the level of trust between parties. After all, B2B eCommerce will be a $1.1

In the broadest terms, APIs help speed the embrace of Open Banking, where banks’ data on accounts and transactions can be shared with third parties through the interfaces, with an eye on promoting the development of new apps and financial products. The Security Concerns. financial services firms to cross the Open Banking Rubicon. “If

Such disruption and transformation can transcend use cases, said the executive, across B2B, B2C and P2P transactions. So, technology, said Galarza, is indeed changing the actual nature of transactions — down to how they are done at the most basic level.

This new set of APIs offers users a way to “integrate their financial institutions, accounting and enterprise resource planning ( ERP ) systems and their account on GlobalPay,” according to the release. APIs also utilize the latest level of regulated European internet security: strong customer authentication (SCA).

Snap Accounts Payable, otherwise known as SnapAP, has announced the completion of the first stage of funding from angel investors as it continues on its way toward a planned $2 million seed investment round. Italy's Deliveristo secured a $5.51 Deliveristo. million investment, Tech.eu

Investment rounds poured in across Asia, North America and Europe, with a Chinese “corporate wallet” securing the largest investment of the week. The company enables travel providers to not only manage their booking, but it adds an array of back-office services, like inventory management and accounting integrations. FinCompare.

Corporates want to delay payment as long as possible in order to better manage cash flow, while suppliers are pressed to accelerate accounts receivable to strengthen their own cash positions. One of the most prominent culprits behind that friction is the intrinsic conflict that buyers and suppliers face in their payment flows.

In addition, they can spare tenants from fines related to late rental payments by helping them more rapidly move money into their landlords’ accounts. . These tools allow systems to better interact with one another, helping two parties to more securely transmit data. .

There are significant segments of the American consumer base that appreciate the pay-as-you-go aspect, convenience and trusted security of debit,” he said. And security and safety is particularly top of mind with consumers today in the pandemic.”. The Shift To Safety. Use of debit in eCommerce has accelerated during the pandemic.

28) that shares of the eCommerce firm Infibeam Avenues Ltd plunged 71 percent after a WhatsApp message “circulated among traders” centering on the company’s accounting methods, causing holders to flee its stock. Bloomberg reported Friday (Sept. Per Bloomberg, that message said the company had given interest-free loans to its own units.

The company also said digital accounts can be used to activate and tokenize other digital accounts across various mobile pay wallets. In the April Digital Consumer Onboarding Tracker , PYMNTS explores how players from around the world are taking new approaches to onboarding security.

B2C trends are bleeding into the B2B space and forcing corporate sellers to become digitally savvy — and fast. Sellers seeking to fend off such scams need to differentiate fake accounts from legitimate ones. False Positives and Data Security. No anti-fraud strategy is a cure-all, however, and even security measures bring risks.

She noted that firms such as PULSE have enabled payments functionality spanning push payments, peer-to-peer (P2P) and business-to-consumer (B2C) for the past decade and that operating rules require funds to be available in customer accounts within 30 minutes.”. The Security Angle.

Some are currently available and some deployments are in process or development, including benefits AI can bring to the intellectual property landscape.IX

MC Payment offers an array of B2C and B2B payment solutions, but its most recent offering is Xaavan, a B2B supply chain payments and eInvoicing platform. Though averaging about $1 million per loan, the company said it has just secured a $10 million line of credit for a borrower, its largest to date. 17) that it secured $1.81

Customers, on the other hand, need to be assured that their PII, such as credit card or bank account numbers, will remain safe. . The movement of money is initiated when the merchant’s bank requests to “pull” money out of the customer’s account and place it into the merchant’s. B2C push payments can deliver quick funds to consumers.

Malaysia's microLEAP has secured $3.3 The company offers automated accounting solutions, accounts receivable solutions like payment reminders and invoice generation, expense management and other tools for small and medium-sized businesses (SMBs) to manage finances.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content