This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And while the coronavirus pandemic has thrust traditional B2B suppliers into a state of uncertainty, Spear noted that there are opportunities to emerge from the volatility by transforming accounts receivable (AR) and trade credit processes. B2C Sellers’ B2B Incentive. Optimizing Ad-Hoc Procurement.

Being able to track the flow of funds and correctly auto-post those funds to an invoice-level based accounts receivable (AR) system, said Diegelman, can be difficult. As a result, a number of disconnected data streams become a single thread that is the payment’s life history from point A to point B.

Corporates are being forced to rethink their approach to accounting as new technologies disrupt the way firms transact and manage financialdata. But, tools like electronic payments and cloud accounting software are far from the only forces that alter the corporate accounting landscape.

In the broadest terms, APIs help speed the embrace of Open Banking, where banks’ data on accounts and transactions can be shared with third parties through the interfaces, with an eye on promoting the development of new apps and financial products. financial services firms to cross the Open Banking Rubicon. “If

In a recent report , seed investors explored why their focus has turned to enterprise startups as opposed to consumer-facing technology firms after the publication’s analysis revealed that today’s seed investments favor B2B startups over B2C. Receipt Bank. HighRadius. The leader of the B2B pack this week is U.S.-based

CFOs are often asked to oversee additional functions on top of traditional finance and accounting." He takes note that front-end B2C systems such as CRM, and supply chain enablement systems such as QR codes can be of help for channel inventory tracking. "‘Partnering’ is nothing new," says Ho.

“Three quarters of all B2B transactions still happen through paper or PDF,” notes Galarza, and require the need for both an accounts receivable and an accounts payable department. Meanwhile, in a B2C transaction, “the consumer can simply pull up their credit card to pay for goods and services.”. Australia … the U.K.,

As instant payment schemes continue to roll out across the world, this not only impacts B2C companies, but also has a knock-on effect on the full value chain of globally connected corporates,” said Deutsche Bank Head of Cash Products, Global Transaction Banking Shahrokh Moinian in a statement announcing the report.

As B2B eCommerce grows in popularity among merchants ( BigCommerce data released earlier this month found that 80 percent of merchants accept B2B orders online), companies are less able to ignore their struggle to manage multiple payment rails and payment processors.

California-based SOCi offers SaaS for businesses to manage their social media accounts for marketing and BI purposes. Perfios operates in both the B2B and B2C markets and provides financial institutions and FinTechs with solutions to aggregate and analyze financialdata for the purpose of streamlining loan decision making.

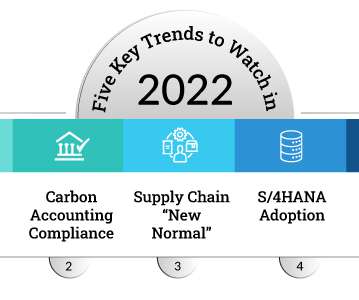

As followers of this blog already know, DSE has been a major disruptive force across many different B2C and B2B markets over the past year and is expected to continue evolving rapidly throughout 2022. This is another subject that we've been tracking closely and have addressed in a recent blog on Carbon Accounting Compliance.

Even if cash has its place, Ferrabee said that digital payments can still gain traction with the addition of information — data, in other words — that can literally travel, and that can be used to ensure (and reassure) both sides of a transaction of speed and security. That’s especially true for corporate and B2C transactions, he said.

And we see that this trend is definitively not restricted to B2C model, while the lines between B2B and B2C are blurring. Leveraging Sustainability Accounting for Competitive Advantage It's clear that new global, national, and local regulations have been a major catalyst for initial ESG implementation.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content