This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Variables The variables that I report industry-average statistics for reflect my interests, and they range the spectrum, with risk, profitability, leverage, and dividend metrics thrown into the mix. Since I teach corporate finance and valuation, I find it useful to break down the data that I report based upon these groupings.

This requires a deep understanding of business processes, industry trends, and how SAP solutions can be leveraged to drive organizational success. At Bramasol, we pride ourselves on being able to "go deep" with our in-house expertise on accountingstandards, industry trends, and emerging challenges that form the big picture for our clients.

However, even though medical equipment leasing bundled with other services and products is making relationships with customers more holistic, the backend systems for handling lease management and accounting have mostly remained in separate silos from those for subscription management and revenue recognition.

Globalization CFOs have long needed to assure compliance with two different standards-setting bodies. The first is the Financial AccountingStandards Board (FASB) in the United States.

Identifies variances and anomalies that don’t comply with accountingstandards with intuitive dashboards and reports that work based on your preset conditions. Best Practices Your accountant is under a lot of pressure at the end of the month to manage the close in a timely manner.

A subsequent blog post specifically addressed How Can Carbon Accounting Impact the Value of M&A Deals? Among the biggest developments is a new proposed rule from the Securities and Exchange Commission (SEC) that was published on March 21, 2022 for public comment over the next 60 days.

Compliance: The adoption of ASC 606 and IRFS 15 accountingstandards for revenue recognition introduced new requirements for SaaS companies, particularly around the allocation of revenues and the recognition of variable consideration.

By leveraging our leadership in deploying more RAR implementations than any other partner, Bramasol is also at the forefront of helping refine and deploy these new Universal RevRec capabilities. Enhanced Compliance : Facilitates adherence to accountingstandards and regulations, reducing the risk of non-compliance and associated penalties.

The growing variety and complexity of tasks within the finance function has resulted in the creation of a discipline that is supposed to become a bridge between the finance and business to support decision-making process by leveraging data and technology. This relates to FP&A which stands for financial planning and analysis.

Covenant Threshold Monitoring To avoid any risk of breaching any covenants, the system monitors the current status against periodic covenant tests for earnings, leverage, liquidity, or other metrics dictated by lending agreements. Alerts notify appropriate stakeholders as threshold limits approach.

The Big Four auditing firms — EY, Deloitte, KPMG and PwC — have recently requested that the Financial AccountingStandards Board (FASB) provide clarity in how corporates should classify their reverse factoring or supply chain financing agreements, adding more fuel to a long-standing debate as to whether such trade financing tools are debt.

When choosing the best financial reporting software solution, it's important to consider factors such as ease of use, scalability, integration with existing systems, compliance with accountingstandards, cost, customer support, and any unique requirements your organization might have.

Potential for Growth: Opportunities for South Africa to catch up in terms of leveraging data and technology for economic development. They need to determine how to capitalize intangible assets and ensure compliance with local and international accountingstandards (e.g., Why is this important for CFOs? IFRS, US GAAP).

Solution: Create a Strong Accounting Process Nonprofit leaders can solve this problem by creating and implementing strong internal controls for the organization. You’ll likely want to ask your nonprofit accountant to help you set up your accounting systems so you know they’re correct from the start.

Given the increasing use of accounting software to do day-to-day tasks, accountants need to not just be proficient in accounting, they have to be tech savvy. Accountants deserve positions that leverage technology to improve the department and the organization and when they don’t get that, it creates a challenge.

The financial close process, also known as the accounting close process or month-end close, is a series of steps undertaken by an organization to finalize its financial records for a specific accounting period.

Suppose new accountingstandard requires certain position to use a different basis of valuation. Treasury accountant should be able to go to the equivalent of an “app store” where he can find the appropriate app for this purpose. From what we’ve discussed, customization is the only, sub-optimal solution. C) Why not Apps?

This discrepancy is largely attributable to tax strategies that leverage depreciation and amortization expenses to minimize taxable income , often resulting in a significant gap between NBV and market value early in an asset's life. Income Generation: It should be actively utilized in business operations to generate revenue.

Compliance and Regulation: Financial Planning and Analysis ensures compliance with financial regulations, accountingstandards, and reporting requirements. FP&A identifies areas for cost savings, process improvements, and resource reallocation.

Leverage External Frameworks and Standards Adopt Recognised Reporting Standards: Implement existing frameworks such as the Global Reporting Initiative (GRI), Sustainability AccountingStandards Board (SASB), or the Task Force onClimate-related Financial Disclosures (TCFD) tostructure ESG reporting.

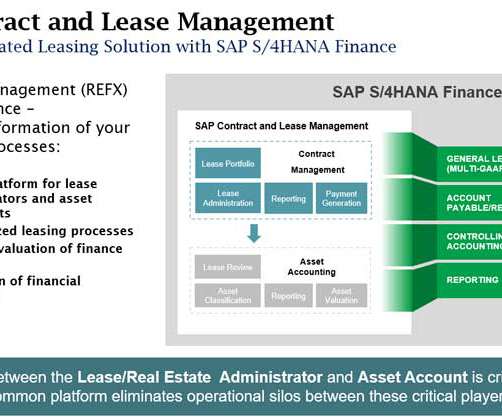

In 2018, the Financial AccountingStandards Board (FASB) and the International AccountingStandards Board (IASB) announced the release of new accountingstandards, ASC 842 and IFRS 16, that redefined how organizations must account for leases.

Leverage Online Learning Platforms Online learning platforms provide excellent opportunities to expand financial knowledge. Courses from platforms like Coursera, Udemy, and LinkedIn Learning offer training in finance, accounting, and business strategy.

He said that “leveraged lending” and “student lending [are] growing rapidly, and deteriorating rapidly.” Dimon offered a cautionary nod toward new accountingstandards that may stifle smaller lenders, such as community banks, if a financial crisis hits again. Others mentioned shadow banks, which are non-bank lenders.

He said that “leveraged lending” and “student lending [are] growing rapidly, and deteriorating rapidly.” Dimon offered a cautionary nod toward new accountingstandards that may stifle smaller lenders, such as community banks, if a financial crisis hits again. Others mentioned shadow banks, which are non-bank lenders.

ASNESS: Ultimately, the shareholders, I won’t go through all the other subtleties, what’s a little sad is we kind of won the battle in that current accountingstandards make you expense stock options and that was a change. RITHOLTZ: They have that. I think the short termism can be exaggerated. They can raise money in debt.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content