This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

IFRS 16, published by the International AccountingStandards Board (IABS), came into effect on January 1, 2019. Most organizations operating in Asia Pacific are aware of this new standard but may not be aware of a better way to make the transition.

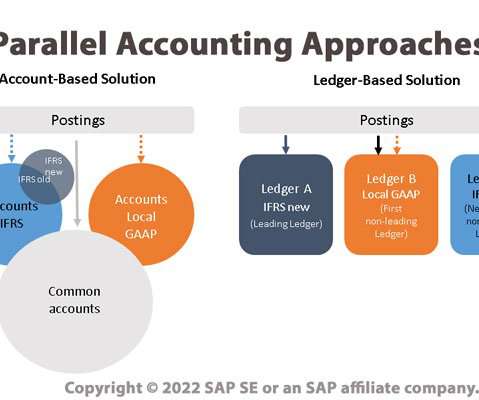

One important side effect of the ongoing trend toward globalization is the need to comply with a range of different accounting principles as well as with disparate reporting and compliance mandates. Parallel Ledgers - in which multiple ledgers are used, with an accounting principle applied to each ledger. Asset Accounting (FI-AA).

Globalization CFOs have long needed to assure compliance with two different standards-setting bodies. The first is the Financial AccountingStandards Board (FASB) in the United States. IFRS S1 requires companies to communicate the sustainability risks and opportunities they face over the short, medium, and long term.

In addition, global companies need the flexibility to comply and report according to multiple accountingstandards. For leasing, this means International AccountingStandards Board’s (IASB’s) IFRS 16 and US GAAP Financial AccountingStandards Board’s (FASB’s) ASC 842.

The Need for Specialized Technology Solutions To address this pressing need, treasury teams are relying on CS Lucas Treasury Management System’s dedicated syndicated loan modules. Let’s explore some of the key capabilities of CS Lucas: 1. Management and auditors gain on-demand reporting.

So a lot of invoices, accounts payable, accounts receivable, cash flow management, treasury working with procurements, so really the back office function at Anheuser-Busch, really pushing, making sure that everything works efficiently. So a lot of it was leading back office finance for the company.

One reason is that these businesses are not only not required to publicly disclose their financial details in most parts of the world, but often follow more malleable accountingstandards, making the data less reliable and comparable.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content