This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Since the release of new lease accountingstandards ASC 842 and IFRS 16 in 2018, companies have taken a variety of approaches to comply, but many are now aiming to optimize their lease accounting processes for efficiency and long-term manageability.

In 2018, the Financial AccountingStandards Board (FASB) and the International AccountingStandards Board (IASB) announced the release of new accountingstandards, ASC 842 and IFRS 16, that redefined how organizations must account for leases.

Globalization CFOs have long needed to assure compliance with two different standards-setting bodies. The first is the Financial AccountingStandards Board (FASB) in the United States. IFRS S1 requires companies to communicate the sustainability risks and opportunities they face over the short, medium, and long term.

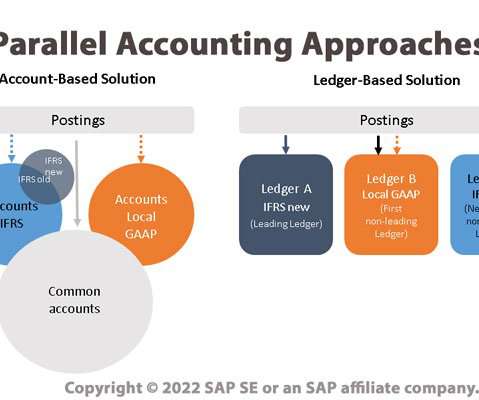

One important side effect of the ongoing trend toward globalization is the need to comply with a range of different accounting principles as well as with disparate reporting and compliance mandates. Parallel Ledgers - in which multiple ledgers are used, with an accounting principle applied to each ledger.

In addition, global companies need the flexibility to comply and report according to multiple accountingstandards. For leasing, this means International AccountingStandards Board’s (IASB’s) IFRS 16 and US GAAP Financial AccountingStandards Board’s (FASB’s) ASC 842.

SAP Universal Revenue Management (SAP Universal RevRec) is a cutting-edge solution engineered to elevate and simplify the complexities of revenue recognition. Enhanced Compliance : Facilitates adherence to accountingstandards and regulations, reducing the risk of non-compliance and associated penalties.

A subsequent blog post specifically addressed How Can Carbon Accounting Impact the Value of M&A Deals? From a global perspective, the International Sustainability Standards Board (ISSB) is also working on developing uniform financial reporting rules.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content