This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It can quickly become unmanageable to try and handle lease contract management, lessor accounting, maintenance services, sales of consumables, revenue recognition and disclosure reporting all with different siloed software. In addition, global companies need the flexibility to comply and report according to multiple accountingstandards.

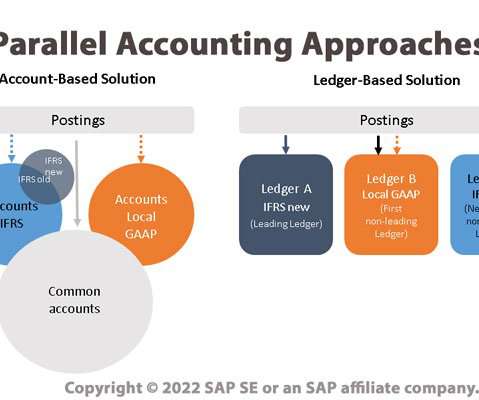

One important side effect of the ongoing trend toward globalization is the need to comply with a range of different accounting principles as well as with disparate reporting and compliance mandates. Parallel Ledgers - in which multiple ledgers are used, with an accounting principle applied to each ledger.

Reports in The Block Crypto late last week said a group of California CPAs has sent a letter to the Financial AccountingStandards Board, a federal board that sets Generally Accepted Accounting Principles (GAAP), requesting that it consider establishing a task force to address a lack of clarity in cryptocurrency accountingstandards.

AI in the “Real World” While these powerful tools seem to have a near mastery of natural language communication, they are not necessarily designed to possess many of the skills required by finance and accounting professionals. They’re not very good at mathematics or dealing with numbers in general.

However, the revenue recognition guidance offered under US GAAP vs. IFRS has differed and was in need of improvement. So for a number of years, the Financial AccountingStandards Board (FASB) and the International AccountingStandards Board (IASB) have been working to converge their guidelines for revenue recognition.

Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting. As a result, the organization might not adhere to Generally Accepted Accounting Principles (GAAP), which can trip them up come tax time or during an audit. Improves compliance.

One way to ensure you remain within the confines of your tax-exempt status is to file and share a number of financial statements. You have a primary responsibility to your donors, grantmakers, and other stakeholders to find ways to share these statements while still following the highest accountingstandards.

AI in the “Real World” While these powerful tools seem to have a near mastery of natural language communication, they are not necessarily designed to possess many of the skills required by finance and accounting professionals. They’re not very good at mathematics or dealing with numbers in general.

This measure is a direct product of fair value reporting, a principle insisting that assets be reported at their market value, which forms the bedrock of financial reporting standards under US GAAP. Determining Eligibility for Depreciation To accurately apply depreciation, it is essential to first determine which assets are eligible.

In closing, I also want to dispense with the notion that data is objective and that numbers-focused people have no bias. Finally, it is worth noting that, notwithstanding the travails of last year, the number of firms in the data universe increased from 44,394 firms at the start of 2020 to 46,579 firms, a 4.9%

Pre Series B, it’s a part-time role to simply track past financial numbers. These are complex questions to answer and few companies would have an in-house expert on this subject, especially in light of the new accounting rule for revenue recognition. Their titles include CEO, CTO, COO, CFO, and VP of Finance of venture-backed startups.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content