This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For example, while South African companies follow International Financial Reporting Standards (IFRS), the US requires compliance with its Generally Accepted AccountingPrinciples (GAAP). IFRS is principles-based and allows for some judgment in financial reporting, while GAAP is more rigid, rules-based, and less forgiving.

Such tasks as reconciling accounts, monthly closing, preparing financial statements are part of the accounting cycle and are typically managed by accounting departments. This can lead to burnout, missed deadlines, and a loss of focus on high-value activities.

The profit and loss statement is one of the main parts of the annual statement that companies must prepare at the end of a financial year, along with the cash flow statement and accounting balance sheet. This article discusses influential factors, advantages, and common problems considering the profit and loss statement.

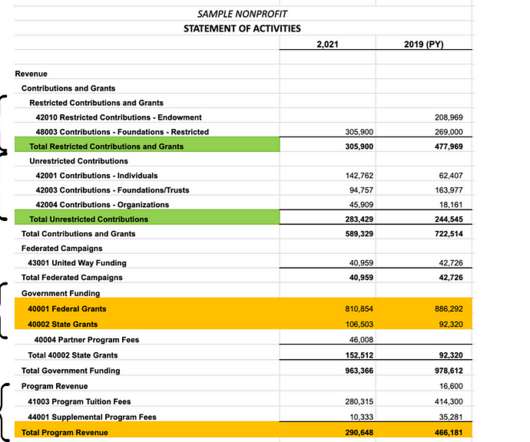

The basic accountingprinciples for nonprofit organizations are the same as accounting for for-profit companies. . So let’s start with the basics, and later we’ll dig into some of the things that make nonprofit accounting unique. . How is nonprofit accounting different? Difference #2: Fund Accounting.

The We Company , the parent of WeWork , uses a cash-flow metric called the “contribution margin,” which showed that its core services were profitable, Bloomberg Tax reported on Tuesday (Dec. The company used generally accepted accountingprinciples (GAAP) to essentially turn a $1.9 billion net loss into a $142 million profit.

In simple terms, that means the cannabis industry taxable income is closer to its revenue rather than profit. The difference between cost of goods sold and ordinary business expenses is well defined in Generally Accepted AccountingPrinciples (GAAP) but routinely ignored by small business bookkeeping services. Interest expense.

You may also know it as a profit and loss statement or income and expense report. In the for-profit world, they call the difference between revenues and expenses net income. Or profit. . It shows you the “profit” of your nonprofit. But here, we call profit a “surplus” instead.

Expansion contributes to a profitable business, but if you don’t prepare to handle rapid growth, you will ultimately hurt your bottom line and prevent your business from reaping the benefits. With split operations, there is an increased risk of inaccurate, error-prone data and a considerable loss of productivity.

For that reason, your account numbering, category names, and structure should follow standard guidelines and numbering conventions established by Generally Accepted AccountingPrinciples (GAAP). . Gain/Loss on Sale of Assets. Gain or loss resulting from the sale of property or equipment. Assets-1000s. Equity-3000s.

Nonprofit organizations distinguish themselves from for-profit entities through their purpose and mission. Their mission is usually anchored on a cause or social purpose, not on the generation of profits. NPOs must adhere to these accounting policies to remain compliant with the law and maintain their tax-exempt status.

Accounting for in-kind donations isn’t just important; it’s required for many nonprofit organizations. . Prepare financial statements per Generally Accepted AccountingPrinciples (GAAP). The estimated market value gets recorded as both revenue and an expense on your profit and loss statement.

The CFO's job is to decipher various departmental forecasts to create profit projections for the CEO and shareholders. It's like looking at the gain or loss you make from an investment compared to what you spent. The CFO plays a key role in ensuring these statements are accurate and in line with standard accountingprinciples (GAAP).

QOE reports go beyond the balance sheet and profit and loss statement – they challenge the underlying data through rigorous testing and management interviews to assess accuracy, and risk. Significant and/or unusual accounting policies such as: Changes in accounting methods. Changes in accountingprinciples.

Start With the Fundamentals of Nonprofit Tax Filing Non-profit organizations operate in many areas of society, including education, healthcare, sports, and social services. Proper revenue recognition is a core accountingprinciple that ensures proper financial reporting, ensuring that you remain compliant and maintain donor confidence.

It is important to accurately track and report unearned revenue, so you can properly manage profit margins. An income statement, also called a Profit and Loss statement (or P&L) records revenue and expenses over time. If revenue is improperly recognized, it will report higher profits than actual.

Compliance: Adherence to accounting standards and regulations, such as Generally Accepted AccountingPrinciples (GAAP) or International Financial Reporting Standards (IFRS). Predefined Reports: Xero provides a variety of standard financial reports, such as profit and loss statements, balance sheets, and cash flow statements.

Pro forma financial statements and GAAP It's important to note that, since pro forma statements are based on hypothetical or projected data, they are not compliant with generally accepted accountingprinciples—GAAP statements must be based on actual financial results.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content