This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The next logical step might be to take your company to international markets by listing on a foreign stock exchange. IFRS is principles-based and allows for some judgment in financial reporting, while GAAP is more rigid, rules-based, and less forgiving. This isn’t just an accounting challenge; it’s a storytelling challenge.

So now is the perfect time to make sure you report in kind gift donations in compliance with GAAP standards in 2022. The changes to in kind donation reporting are specifically for organizations that follow generally accepted accountingprinciples (GAAP) in preparing their financial statements. Who do the changes impact?

The difference between cost of goods sold and ordinary business expenses is well defined in Generally Accepted AccountingPrinciples (GAAP) but routinely ignored by small business bookkeeping services. Even worse, an IRS income tax return does not follow the same rules as GAAP. Other distribution expenses, such as rent.

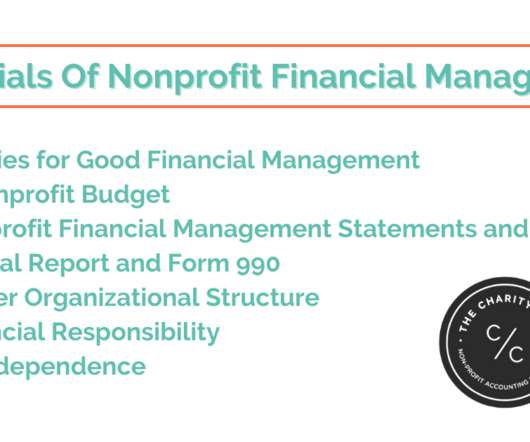

The basic accountingprinciples for nonprofit organizations are the same as accounting for for-profit companies. . So let’s start with the basics, and later we’ll dig into some of the things that make nonprofit accounting unique. . Accounts Payable. Nonprofit accounting has its own terminology.

Accounting for in-kind donations isn’t just important; it’s required for many nonprofit organizations. . Prepare financial statements per Generally Accepted AccountingPrinciples (GAAP). For the purposes of GAAP, donations of goods and services are valid revenue. Step #1: Establish Fair Market Value .

Reports in The Block Crypto late last week said a group of California CPAs has sent a letter to the Financial Accounting Standards Board, a federal board that sets Generally Accepted AccountingPrinciples (GAAP), requesting that it consider establishing a task force to address a lack of clarity in cryptocurrency accounting standards.

They prepare the income statement, balance sheet, and statement of cash flows using the accrual accounting method. Familiarity with Generally Accepted AccountingPrinciples (GAAP) is essential.

Safra Ada Catz Safra Ada Catz, the business leader overseeing ,, Oracle Corporation , a major tech company, handles key aspects like sales, marketing, finance, and legal matters. As CFO and co-president at Goldman Sachs, he oversaw financial operations and drove strategic initiatives, expanding into new markets. as its CFO.

The PCAOB and AICPA essentially interpret and enforce accounting rules as promulgated by the Financial Accounting Standards Board (FASB) , which is responsible for establishing and improving accounting standards for financial reporting in the United States.

If there are, for example, high marketing expenses, it may be necessary to explore ways to reduce those costs. It’s easy to forget to include all of the expenses associated with running an organization, such as marketing, repairs, or travel costs. Identifying areas of improvement. Omitting expenses. Inaccurate revenue.

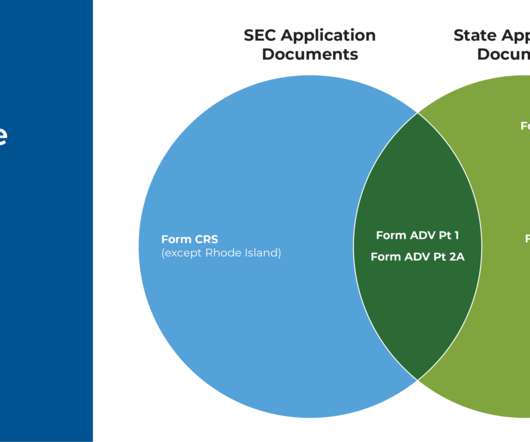

Along with renewing their registration annually (for both SEC- and state-registered firms), firms face a variety of requirements related to their internal finances, fees, marketing activities, and advisor agreements depending on whether they are SEC- or state-registered. RIA Marketing Activities (Including Testimonials).

When creating your fiscal policy, ensure that it complies with the Generally Accepted AccountingPrinciples (GAAP). Bring GAAP compliance. Create transparency and accountability required by the board and IRS. It helps to: Market your mission. A Nonprofit Budget. Ease the tax reporting. Thank your donors.

Is your business set up to handle these dynamic market conditions? Or perhaps your integrated cash flow reports are based on GAAPaccountingprinciples rather than formulas, but your existing planning and forecasting software application doesn't support them. Do you have the resources to adapt?

The answers—based on different sources of data like market research or historical sales information—guide internal decision-making to promote regular, sustainable growth as well as create contingency plans for worst-case or best-case scenarios. While GAAP statements are required for public companies, pro forma financials are not.

Accounting Standards In the United States, all organizations must adhere to the Generally Accepted AccountingPrinciples (GAAP). This establishes core accounting standards for nonprofits which help with accountability and transparency.

If your company’s accountant can’t keep up with the workload, a controller would be more beneficial than a second accountant, and more directly involved than a CFO who is probably not needed in this situation. This encompasses investors, growth, expectations, and market outlook, creating the need for a CFO much earlier than before.

This accountingprinciple offers an insightful perspective into a business's worth , underlining the importance of financial reporting in today's market dynamics. Its relation to depreciation highlights why NBV generally falls below the market value in the initial years of an asset's lifespan.

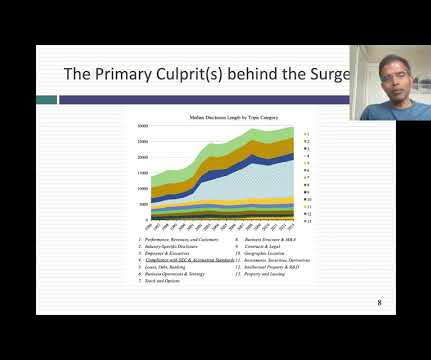

Some of this surge can be attributed to companies becoming more complex and geographically diversified, but much of it can be traced to increased disclosure requirements from accounting rule writers and market regulators. trillion, five times larger than the entire hotel market's revenues in that year.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content