This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In connection with this, the Association of Chartered Certified Accountants is urging businesses to take steps to maximise the opportunities of AI and lay foundations for responsible use of new technologies. Technology has long been a game-changer for accounting. The post Seizing opportunities in finance appeared first on FutureCFO.

Members’ Profile: Rofhiwa Irene Singo In this edition of our CFO Spotlight series, we are featuring Rofhiwa Irene Singo, an accomplished finance leader whose journey is a testament to resilience, adaptability, and impactful leadership. What sparked your interest in finance?

How a CFO Ensures Compliance in FinancialReporting Reliable financial statements are crucial for business management, but ensuring compliance may feel like a luxury in the resource-constrained world of small business. What is Financial Statement Compliance? This should include regular workshops and seminars.

Finance organizations regularly face the challenges of meeting strict deadlines and satisfying data quality requirements for closing the books and delivering accurate financial statements. IBM Cognos Controller supports the close, consolidation and reporting process with the agility and affordability of a cloud-based solution.

While the number of mistakes has declined every year since 2006, during the first six months of 2018, 65 companies found accounting mistakes that required them to restate and refile entire financial filings, compared with 60 companies for the same period last year. tax law and revenue accounting rules.

Corporate accounting standards are changing, with the FinancialAccounting Standards Board adopting new standards in ways companies report on leases, hedging and other financial activity. ” Meanwhile, previous research from Audit Analytics has also revealed that the number of accounting errors among the U.S.’s

(GOOGL) stock worth over $20 million, his financial portfolio is quite diversified. Anthony Noto Anthony Noto, a famous finance executive and former NFL exec, now wears the CEO and CFO hats at a fintech company named SoFi. His main job is to handle all money matters at SoFi, like planning, accounting, and dealing with investors.

In an ideal world, financialreports should build shareholder trust by offering accurate data about the performance of the company. In reality, a company’s financialreport can be more flimsy—involving estimates and judgment from leadership that’s far from the truth. at its peak to $0.26

If you’re like most nonprofit leaders, you’re not researching nonprofit accounting basics to satisfy your curiosity. You need to get a better grasp of your organization’s finances now. So you can understand what’s happening in your business and communicate effectively with your board members, donors, and financial team.

The changes to in kind donation reporting are specifically for organizations that follow generally accepted accountingprinciples (GAAP) in preparing their financial statements. And the second will impact the information you include in your disclosures (footnotes) to your financialreports.

Overview of the PCAOB and AICPA The Public Company Accounting Oversight Board (PCAOB) is a regulatory body established by the Sarbanes-Oxley Act of 2002 in response to corporate accounting scandals like Enron and WorldCom. Why Should You Care?

But that’s not quite true—nonprofits face a decision between 2 different accounting methods for tracking their financial activity: cash accounting vs. accrual accounting. Though both systems use the same numbers, looking at those numbers differently can give you a very different perspective on the state of your finances.

All these sources must be carefully managed to ensure compliance with Generally Accepted AccountingPrinciples (GAAP) and guidelines. Understanding how and when to recognize different revenue is perhaps one of the most important but difficult aspects of managing a nonprofit’s finances. Get the free guide!

This makes it challenging to create technology that tracks data for fundraising purposes while still following accountingprinciples. This makes it difficult to maintain the integrity of both donor and financial records when attempting to sync the two systems. Do You Struggle to Make Sense of Your Financial Statements?

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted AccountingPrinciples (GAAP) and FinancialAccounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

For example, “salary” is a straightforward line-item on a for-profit financialreport. . To complete your IRS 990, you’ll need to report your expenses based on how they fall within 3 categories, they are: . That means you’ll need to present a Functional Expense Report to pass an audit. To build public trust.

But did you know there are a variety of financial professionals that are essential to the financial well-being of an organization? Bookkeepers, accountants, and Chief Financial Officers (CFOs) all serve critical roles in managing an organization’s finances. What is a Bookkeeper? Get the free guide!

A financial statement audit is a thorough review of your financial statements to determine if your financial statements present fairly, in all material respects, in accordance with generally accepted accountingprinciples. The purpose of a financial statement audit is NOT to detect fraud.

CFOs rely on robust finance and accounting expertise, backed by years of experience, to boost the organization's financial health. In their capacity, CFOs usually: Engage with departments such as accounting, customer service, and finance. Address accounting and finance issues.

In the United States, these Generally Accepted AccountingPrinciples (or GAAP) are set by the FinancialAccounting Standards Board (FASB). NPOs must adhere to these accounting policies to remain compliant with the law and maintain their tax-exempt status. Do You Struggle to Make Sense of Your Financial Statements?

While many nonprofits start with cash-basis accounting due to its simplicity, this method often falls short of providing a comprehensive view of a nonprofit’s financial health. Transitioning to accrual-basis accounting can offer a more accurate representation of finances and enhance long-term planning. Get the free guide!

Episode 243 Becoming a Treasurer Series, Part 24: Languages of Finance: FP&A As we jump back into the Becoming a Treasurer series, we are launching a new sub-series where we will look at the “language of finance.” What are some of the different ways we look at it in finance, accounting as a view of it?

Whether you are an educational, charitable, religious, sports, or other public-benefit organization, you need to have a good handle on your finances in order to make the most impact. Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting.

In the quest for efficiency and accuracy in finance, AI bookkeeping emerges as a promising solution. Consistency: By minimizing human error, AI ensures a stable and standardized bookkeeping process, crucial for maintaining consistent financial records. But does it truly live up to its promise?

To maintain good governance practices and requirements To demonstrate financial transparency to your donors, members, and the public To make sure that your organization complies with the taxman, you should file IRS Form 990 by May 15 each year. Do You Struggle to Make Sense of Your Financial Statements? Get the free guide!

Accounting Standards In the United States, all organizations must adhere to the Generally Accepted AccountingPrinciples (GAAP). This establishes core accounting standards for nonprofits which help with accountability and transparency. Do You Struggle to Make Sense of Your Financial Statements?

Understanding the Net Book Value (NBV) of a company's assets is critical for knowing its financial health and potential for future growth. This accountingprinciple offers an insightful perspective into a business's worth , underlining the importance of financialreporting in today's market dynamics.

But in the accounting world, “financial consolidation” is a well-defined process that includes several complexities and accountingprinciples. Here are the key accounting consolidation steps in the finance consolidation process : Collecting trial balance data (e.g.,

FP&A candidates typically have a background in finance, accounting, or a related field and possess a combination of skills and knowledge in financial analysis, modeling, and strategic planning. Problem-Solving: The ability to identify financial challenges and propose solutions is crucial.

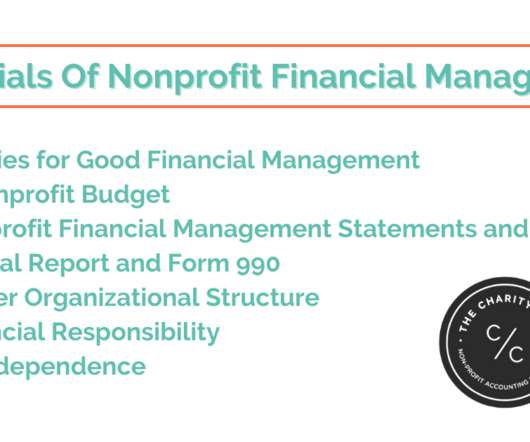

Many nonprofit organizations tend to let their financial management slip on the backburner as they get busy fulfilling their mission. Sure, your mission should be a priority, but managing finances can’t be neglected either. Without a good grasp of your finances, your nonprofit risks: Exposure to fraud. A Nonprofit Budget.

Universal Parallel Accounting (UPA) Universal Parallel Accounting (UPA) provides a harmonized architecture for ledgers and currencies, which enables a foundation for not only calculating and posting values per ledger and currency along end-to-end processes, but also provides the baseline for future innovations in finance.

If a company fails to accurately record its unearned revenue, it could lead to inaccurate financialreporting and create potential legal issues. If revenue is improperly recognized, it will report higher profits than actual.

Pro forma statements are financial projections that ask and attempt to answer "what if" questions. What will our finances look like?" The Securities and Exchange Commission (SEC) requires that discrepancies between pro forma and GAAP-compliant financialreports be explained when released to the public.

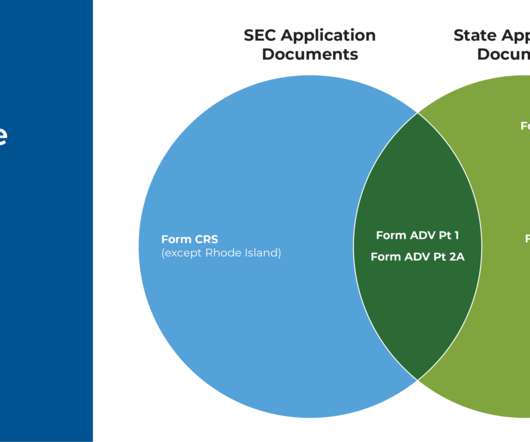

Along with renewing their registration annually (for both SEC- and state-registered firms), firms face a variety of requirements related to their internal finances, fees, marketing activities, and advisor agreements depending on whether they are SEC- or state-registered.

If shortfalls are projected, proactively develop strategies to address them, such as securing additional financing or adjusting expenses. Building an emergency fund can provide a cushion during challenging times and reduce reliance on external financing. Optimize Cash Flow: Identify opportunities to enhance your cash flow.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content